Dear Students,

The second semester has almost come to an end. I enjoyed my classes with you. As I was teaching you English, I was also learning many things from you. I thank every one for attending my classes in full attendance most of the times. It is my turn to thank you all and wish you the very best for your success in life.

With best wishes

S P Dhanavel

Monday, May 19, 2008

Third Assessment Attendance and Marks

Dear Students,

You have the attendance and marks detals for the third assessment here.

Sl No

Roll No.

Name

Attendance –18

Marks --100

1

20071401

Abinav Santhosh D

17

80

2

20071402

Anitha V

18

68

3

20071403

Bernard Felix C

17

100

4

20071404

Bhuvaneshvari S

15

63

5

20071405

Deepak K

17

83

6

20071406

Deepika B

17

85

7

20071407

Dharmaraj D

AAA

AAA

8

20071408

Dinesh Kumar V

18

83

9

20071409

Feroz Khan M

17

73

10

20071410

Gopi R

17

65

11

20071411

Goutham C

15

73

12

20071412

Haresh G

14

85

13

20071413

Harish S

16

50

14

20071414

Manoj H

18

78

15

20071415

Muthuraj N

18

50

16

20071416

Nagarajan R M R

18

100

17

20071417

Natchammai Revathy P

17

88

18

20071418

Naveen N

18

83

19

20071419

Nethirajan B

12

50

20

20071420

Parthiban D

16

85

21

20071421

Pradeep Kannan M

18

78

22

20071422

Rajkumar T

15

60

23

20071423

Rajshree R

18

85

24

20071424

Ramachandra Venkatarman

15

90

25

20071425

Ramesh G

17

50

26

20071426

Ranjithkumar E

17

58

27

20071427

Reena S

18

60

28

20071428

Romit Kris Sriram

17

100

29

20071429

Rubesh P

15

68

30

20071430

Sahitya K

18

85

31

20071431

Santhish Kumar P R

18

55

32

20071432

Sathish K

15

50

33

20071433

Sathishkumar M

16

83

34

20071434

Sharvan Vaidianath

AAA

AAA

35

20071435

Sriram S

10

73

36

20071436

Subramanian V

18

53

37

20071437

Sureshkumar D

17

78

38

20071438

Suresh K

18

50

39

20071439

Velladurai U

15

53

40

20071440

Vinoth G

16

73

41

20071441

Vivek D

16

78

42

20071442

Mahidar Karan G

13

88

43

20071443

Ajay Gurudev

17

AAA

B.E Manufacturing II Semester 2008, III Assessment Test

Dr S P Dhanavel, AP/English, English II HS 181

You have the attendance and marks detals for the third assessment here.

Sl No

Roll No.

Name

Attendance –18

Marks --100

1

20071401

Abinav Santhosh D

17

80

2

20071402

Anitha V

18

68

3

20071403

Bernard Felix C

17

100

4

20071404

Bhuvaneshvari S

15

63

5

20071405

Deepak K

17

83

6

20071406

Deepika B

17

85

7

20071407

Dharmaraj D

AAA

AAA

8

20071408

Dinesh Kumar V

18

83

9

20071409

Feroz Khan M

17

73

10

20071410

Gopi R

17

65

11

20071411

Goutham C

15

73

12

20071412

Haresh G

14

85

13

20071413

Harish S

16

50

14

20071414

Manoj H

18

78

15

20071415

Muthuraj N

18

50

16

20071416

Nagarajan R M R

18

100

17

20071417

Natchammai Revathy P

17

88

18

20071418

Naveen N

18

83

19

20071419

Nethirajan B

12

50

20

20071420

Parthiban D

16

85

21

20071421

Pradeep Kannan M

18

78

22

20071422

Rajkumar T

15

60

23

20071423

Rajshree R

18

85

24

20071424

Ramachandra Venkatarman

15

90

25

20071425

Ramesh G

17

50

26

20071426

Ranjithkumar E

17

58

27

20071427

Reena S

18

60

28

20071428

Romit Kris Sriram

17

100

29

20071429

Rubesh P

15

68

30

20071430

Sahitya K

18

85

31

20071431

Santhish Kumar P R

18

55

32

20071432

Sathish K

15

50

33

20071433

Sathishkumar M

16

83

34

20071434

Sharvan Vaidianath

AAA

AAA

35

20071435

Sriram S

10

73

36

20071436

Subramanian V

18

53

37

20071437

Sureshkumar D

17

78

38

20071438

Suresh K

18

50

39

20071439

Velladurai U

15

53

40

20071440

Vinoth G

16

73

41

20071441

Vivek D

16

78

42

20071442

Mahidar Karan G

13

88

43

20071443

Ajay Gurudev

17

AAA

B.E Manufacturing II Semester 2008, III Assessment Test

Dr S P Dhanavel, AP/English, English II HS 181

Saturday, May 3, 2008

Care less youth runs over aged cyclist

An old man died in a road accident yesterday evening near Anna university front gate.

The old man who was cycling on the road side was hit by a careless youth in a car . The driver of the car did not stop after hitting the cyclist .A couple of students who witnessed the accident chased the culprit.The college students who were present at the spot, noted the car number and informed the traffic police who joined the students in pursuit of the culprit. The cops hold of the culprit near Adayar signal and was arrested

According to the police report the cyclist was Mr.M.Kumaran(58) was working as a security at state bank ,guindy branch.The old man was on his way back home. M Prabakhar(24) a young I.T professional,working in tidal park was on his way to a party .The driver of the car had to attend a call while he was driving .When the driver of the car tried to reach his mobile ,lost control of the vehicle and ran over the cyclist .He was arrested by the M.Muthuvel , sub inspector at Adayar police station.The careless driver was remanded for judicial custody

by N.Naveen

An old man died in a road accident yesterday evening near Anna university front gate.

The old man who was cycling on the road side was hit by a careless youth in a car . The driver of the car did not stop after hitting the cyclist .A couple of students who witnessed the accident chased the culprit.The college students who were present at the spot, noted the car number and informed the traffic police who joined the students in pursuit of the culprit. The cops hold of the culprit near Adayar signal and was arrested

According to the police report the cyclist was Mr.M.Kumaran(58) was working as a security at state bank ,guindy branch.The old man was on his way back home. M Prabakhar(24) a young I.T professional,working in tidal park was on his way to a party .The driver of the car had to attend a call while he was driving .When the driver of the car tried to reach his mobile ,lost control of the vehicle and ran over the cyclist .He was arrested by the M.Muthuvel , sub inspector at Adayar police station.The careless driver was remanded for judicial custody

by N.Naveen

A rose is plucked before it blooms

A young boy named Shiva,whose age is just 16 years met with an accident near the Anna University signal.This accident took place on 29th April,2008 in the early morning and the boy was spot dead.A drunk lorry driver came in the wrong way and he was the sole responsible for this accident.The boy was in 10th std and his family really lost one earning hand.The Police and other officials are in search of the lorry driver.They have also enforced the rules and punishments to avoid these accidents that occured due to carelessness.

Monday, April 28, 2008

An Unforgettable Session of Life Time with Prof.Mahadevan sir

Hello friends it was on the morning of 25th April 2007, I came to college in a hurry amidst the vechicle crowded trafficous roads of chennai. On reaching the college i was directed by my class representative to go to Henry Mauldslay Hall in the Mechanical Dept. I could not understand why this guy is telling us to go there. And later reaching there i found one of favorite teacher, my english sir Dr. Dhanavel sitting under the tree opp. to the hall welcoming us with a ever smiling face. He took our attendence and directed us to fill the registration form and enter the hall. And finnaly I went to the hall, everyone in the hall were curious to know whats going to happen, then came our English HOD, with a mic in her hand. She told that this session is going to be an unforgettable session in your lives. Then I understood that something is going to happen. Then entered the hall a respectable man with a spanish beard, wearing a blue coat. I thought tat he must be some person from someother state. But he started his speach in our mother toungue tamil. He introdued himself as Mr.Mahadevan sory Mr.P.Mahadevan, where that P stands for "perfect". He told that he is memory specialist and a trainer for the Guiness Book of world records, and that he has trained around 85 students to that. He just called me and asked for my name and i proudly said "my name is Parthiban sir"..It went on like this and he gave some tips. In the middle he called his disciple and demonstrated a memory techniche, he told 30 of us to give 30 different objects and after some time he told us to query her with those 30 objects randomly, to my surprise she told the things exactly even without a small mistake in the things. In the winding up of the session he told that he is going to show us some extraordinary thing. What he did was he told incident of a birth of child that was about 18years old at the end of that i realised that it was my date of birth and it was me whom he was telling about. After that he kept on answering the DOB's of the students and to our surprise he was able to answer everyone. Then he told that its all by consistant practise. Then he told about the program that our Vice-Chancellor requested him to organise. And thats how we ended that session. It was an unforgettable session.

CALL FOR MORE INTERACTION ON THE BLOG

Dear Students,

You may be busy with your assessment tests and end semester practical examinations. Even then do spare some time to visit your blog and post comments and new posts. Only through constant interaction through the blog, the blog will grow with you. You attended the seminar on memory improvement and life enahancement conducted by Mr P Mahadevan. You could share your views on such happenings in your campus.

Let me hope more students will participate in this web communication.

S P Dhanavel

You may be busy with your assessment tests and end semester practical examinations. Even then do spare some time to visit your blog and post comments and new posts. Only through constant interaction through the blog, the blog will grow with you. You attended the seminar on memory improvement and life enahancement conducted by Mr P Mahadevan. You could share your views on such happenings in your campus.

Let me hope more students will participate in this web communication.

S P Dhanavel

Friday, April 11, 2008

Thursday, April 10, 2008

WHY IS TAMIL NEW YEAR CELEBRATED ?

Puthandu, more frequently known as the Tamil New Year and Vishu are celebrated on the same day respectively in the Southern Indian states of Tamil Nadu and Kerala. They generally fall on 13 April or 14 April. The Tamil New Year is celebrated on the first day of the Hindu Solar Calendar. Every year in the month of Chithrai (the first month of the Hindu solar calendar), in the temple city of Madurai, the Chithrai Thiruvizha is celebrated in the Meenakshi Temple. A huge exhibition is also held, called Chithrai Porutkaatchi. In some parts of Southern Tamil Nadu, it is also called Chithrai Vishu. The day is marked with a feast in Hindu homes and entrances to the houses are decorated elaborately with kolams.

On the Tamil New Year's Day, a big Car Festival is held at Tiruvadamarudur near Kumbakonam. Festivals are also held at Tiruchirapalli, Kanchipuram and many other places.

In a recent Assembly Resolution, Tamilnadu Government has resolved that henceforth, January 14th of every year will be celebrated as Tamil New Year's day in addition to the famous harvest festival Pongal. But the said resolution has no public support. It has to be seen whether in due courese, the above move denies April 13/14 the festival colour enjoyed by it for time immemorial.

HAPPY TAMIL NEW YEAR !!

On the Tamil New Year's Day, a big Car Festival is held at Tiruvadamarudur near Kumbakonam. Festivals are also held at Tiruchirapalli, Kanchipuram and many other places.

In a recent Assembly Resolution, Tamilnadu Government has resolved that henceforth, January 14th of every year will be celebrated as Tamil New Year's day in addition to the famous harvest festival Pongal. But the said resolution has no public support. It has to be seen whether in due courese, the above move denies April 13/14 the festival colour enjoyed by it for time immemorial.

HAPPY TAMIL NEW YEAR !!

Tuesday, April 8, 2008

Second Assessment Marks for English II HS 181

Sl No

Roll No.

Name

Attendance –25

Marks --100

1

20071401

Abinav Santhosh D

21

75

2

20071402

Anitha. V

23

73

3

20071403

Bernard Felix C

21

78

4

20071404

Bhuvaneshvari S

25

55

5

20071405

Deepak K

25

73

6

20071406

Deepika B

25

95

7

20071407

Dharmaraj D

AAA

AAA

8

20071408

Dinesh Kumar V

23

80

9

20071409

Feroz Khan M

20

65

10

20071410

Gopi R

21

85

11

20071411

Goutham C

22

80

12

20071412

Haresh G

23

80

13

20071413

Harish S

20

60

14

20071414

Manoj H

24

83

15

20071415

Muthuraj N

15

53

16

20071416

Nagarajan R M R

25

93

17

20071417

Natchammai Revathy P

25

95

18

20071418

Naveen N

25

83

19

20071419

Nethirajan B

21

53

20

20071420

Parthiban D

25

70

21

20071421

Pradeep Kannan M

18

75

22

20071422

Rajkumar T

20

83

23

20071423

Rajshree R

24

73

24

20071424

Ramachandra Venkatarman

22

88

25

20071425

Ramesh G

21

50

26

20071426

Ranjithkumar E

25

80

27

20071427

Reena S

25

83

28

20071428

Romit Kris Sriram

18

80

29

20071429

Rubesh P

24

78

30

20071430

Sahitya K

24

90

31

20071431

Santhish Kumar P R

22

58

32

20071432

Sathish K

20

68

33

20071433

Sathishkumar M

15

68

34

20071434

Sharvan Vaidianath

AAA

AAA

35

20071435

Sriram S

23

75

36

20071436

Subramanian V

25

60

37

20071437

Sureshkumar D

21

93

38

20071438

Suresh K

22

83

39

20071439

Velladurai U

23

65

40

20071440

Vinoth G

20

55

41

20071441

Vivek D

23

85

42

20071442

Mahidar Karan G

25

70

43

20071443

Ajay Gurudev

21

73

B.E Manufacturing II Semester 2008, II Assessment Test

Dr S P Dhanavel, AP/English, English II HS 181

Roll No.

Name

Attendance –25

Marks --100

1

20071401

Abinav Santhosh D

21

75

2

20071402

Anitha. V

23

73

3

20071403

Bernard Felix C

21

78

4

20071404

Bhuvaneshvari S

25

55

5

20071405

Deepak K

25

73

6

20071406

Deepika B

25

95

7

20071407

Dharmaraj D

AAA

AAA

8

20071408

Dinesh Kumar V

23

80

9

20071409

Feroz Khan M

20

65

10

20071410

Gopi R

21

85

11

20071411

Goutham C

22

80

12

20071412

Haresh G

23

80

13

20071413

Harish S

20

60

14

20071414

Manoj H

24

83

15

20071415

Muthuraj N

15

53

16

20071416

Nagarajan R M R

25

93

17

20071417

Natchammai Revathy P

25

95

18

20071418

Naveen N

25

83

19

20071419

Nethirajan B

21

53

20

20071420

Parthiban D

25

70

21

20071421

Pradeep Kannan M

18

75

22

20071422

Rajkumar T

20

83

23

20071423

Rajshree R

24

73

24

20071424

Ramachandra Venkatarman

22

88

25

20071425

Ramesh G

21

50

26

20071426

Ranjithkumar E

25

80

27

20071427

Reena S

25

83

28

20071428

Romit Kris Sriram

18

80

29

20071429

Rubesh P

24

78

30

20071430

Sahitya K

24

90

31

20071431

Santhish Kumar P R

22

58

32

20071432

Sathish K

20

68

33

20071433

Sathishkumar M

15

68

34

20071434

Sharvan Vaidianath

AAA

AAA

35

20071435

Sriram S

23

75

36

20071436

Subramanian V

25

60

37

20071437

Sureshkumar D

21

93

38

20071438

Suresh K

22

83

39

20071439

Velladurai U

23

65

40

20071440

Vinoth G

20

55

41

20071441

Vivek D

23

85

42

20071442

Mahidar Karan G

25

70

43

20071443

Ajay Gurudev

21

73

B.E Manufacturing II Semester 2008, II Assessment Test

Dr S P Dhanavel, AP/English, English II HS 181

Tuesday, April 1, 2008

Non-verbal Communication

Biblical saying: Man does not live by bread alone.

Dhanavel's saying: Man does not communicate by words alone.

Evidence: Albert Mehrabian's book Non-Verbal Communication. 1972.

Communcation takes place as follows: By visual elements -- 55 %

By vocal elements -- 38 %

and by verbal elements -- 7 %

On seeing this everybody should be able to ponder why our communication fails very often. We should look at our own voice and body language more carefully to communicate effectively in future.

Wacth some TV programmes where body and visual language is more prominent than words.

This is one of the best ways for developing non-verbal communication skills.

Best wishes,

S P Dhanavel

Dhanavel's saying: Man does not communicate by words alone.

Evidence: Albert Mehrabian's book Non-Verbal Communication. 1972.

Communcation takes place as follows: By visual elements -- 55 %

By vocal elements -- 38 %

and by verbal elements -- 7 %

On seeing this everybody should be able to ponder why our communication fails very often. We should look at our own voice and body language more carefully to communicate effectively in future.

Wacth some TV programmes where body and visual language is more prominent than words.

This is one of the best ways for developing non-verbal communication skills.

Best wishes,

S P Dhanavel

Saturday, March 29, 2008

ABOUT MYSELF-SATHISH

Iam sathish working as a Manufacturing engineer in Ashok Leyland pvt ltd.i am having the experience of 3 years in Ashok leyland.I had manufactured many new engines and i had a role in bringing a car of worth 90,000 which is great project going on in my company for two years and i assure that i will play role in the best form.soon we are going to introduce in the market with big success

Wednesday, March 26, 2008

ABOUT ME-R@j$!-!rEe

I'm Rajshree . I have just done my bachelor degree in manufacturing engineering in Guindy college of engineering . I'm interested in the of nanotechnology and I have done two projects on robotics . I have done my SAP course in STRIDE Infotech. My special intersts is to do research work in the field of nanotechnology . I wish to carry my further research in your company and I'll try to bring itone among the best companies .

Monday, March 24, 2008

Im posting one of my favourite poems written by the well known poet William Wordsworth `Daffodils`. Its one of the poems which I enjoy till this date Hope you would enjoythe poem.

I wandered lonely as a cloud

That floats on high o'er vales and hills,

When all at once I saw a crowd,

A host, of golden daffodils;

Beside the lake, beneath the trees,

Fluttering and dancing in the breeze.

Continuous as the stars that shine

And twinkle on the milky way,

They stretched in never-ending line

Along the margin of a bay:

Ten thousand saw I at a glance,

Tossing their heads in sprightly dance.

The waves beside them danced, but they

Out-did the sparkling leaves in glee;

A poet could not be but gay,

In such a jocund company!

I gazed—and gazed—but little thought

What wealth the show to me had brought:

For oft, when on my couch I lie

In vacant or in pensive mood,

They flash upon that inward eye

Which is the bliss of solitude;

And then my heart with pleasure fills,

And dances with the daffodils.

That floats on high o'er vales and hills,

When all at once I saw a crowd,

A host, of golden daffodils;

Beside the lake, beneath the trees,

Fluttering and dancing in the breeze.

Continuous as the stars that shine

And twinkle on the milky way,

They stretched in never-ending line

Along the margin of a bay:

Ten thousand saw I at a glance,

Tossing their heads in sprightly dance.

The waves beside them danced, but they

Out-did the sparkling leaves in glee;

A poet could not be but gay,

In such a jocund company!

I gazed—and gazed—but little thought

What wealth the show to me had brought:

For oft, when on my couch I lie

In vacant or in pensive mood,

They flash upon that inward eye

Which is the bliss of solitude;

And then my heart with pleasure fills,

And dances with the daffodils.

ABOUT ME ~ VIVEK

I AM A PROFESSIONAL IN AUTO DESIGN AND MANUFACTURING, AND CURRENTLY SERVING IN THE NATION'S AIR FORCE AS SQUAD COMMANDER IN DEHRADUN. I HAD MY UNDER GRADUATION IN COLLEGE OF ENGINEERING AND AN MBA IN IIM. AM CURRENTLY INVOLVED IN DESIGNING THE NUCLEAR POWERED SUBMARINE WHICH WILL TAKE THE NATION'S DEFENSE TO A NEW HEIGHT. AND I AM ALSO INTERESTED IN HOCKEY AND OTHER FIELD SPORTS. MY BELIEF IN LIFE IS "VICTORIES KEEPS U HIGH,FAILURES KEEPS U LOW BUT ONLY FAITH AND ATTITUDE KEEPS U GOING".

Sunday, March 23, 2008

ABOUT MYSELF-RANJITH KUMAR

I'm Ranjith Kumar, working as a Senior Production Manager in Hero Honda Motors Pvt Ltd.,

me having about 3 years of experience. I handled many projects focused on design and developement .

I specialised in production and desingning softwares.

me having about 3 years of experience. I handled many projects focused on design and developement .

I specialised in production and desingning softwares.

I wish to carry my future works in your esteemeed institution and do my best to your company.

ABOUT ME

I am Anitha.I finished B.E Manufacturing in the College of Engineering,Guindy.I am a very sincere and hardworking person.I have a special interest in the field of politics.I want to do something great to this country.

Saturday, March 22, 2008

About myself-Sahithya

I am currently working as a manager in Ashok Leyland.I have completed my MBA.I also have 3 yrs of working experience.I have done some projects and paper presentations related to my subject.I am also involved in research activities.I would like to join in your prestigious company so that i can work to the best of my ability.I assure you that i bring your company as a tough competitor among the others.

A Page from my forthcoming Biography 'The Perfect Libran'

It was a beautiful evening during the fall in the year 2015. A young energetic Indian graduate from Massachusetts Institute of Technology working for the NASA bumped upon some great idea during his evening stroll,which he did not realise then was goin to revolutionise the area of space travel.

Science had shrunken and now we live in the 'Femto world'.Nagarajan,popularly known as 'Mrinal' among his colleagues was working on 'picotechnology'. The word pico had replaced nano in all fields. Space travel was becoming more and more sophisticated but at the same time more and more complicated. It was at this time he was working with the fuel division in NASA. He struck upon the idea of picofuel cells matrixed in a layer of ceramic, which trapped 905 of solar enrgy and generated power for the shuttle. He presented his paper and got a great deal of appreciation. It as the days when space trave was limited to a particular distance due to fuel cost and expenditure. His idea passed all the prototypes and was asked to present the paper to the President of U.S.A. He approved it and funded 400 billion dollars for the project. he started working on the project and to everyone's surprise he and his team completed the project well ahead of time. The space shuttle with the new technology soared high into the sky during mid-October,2019.

Two years passed by and now he was heading the Far distance Space Exploration Division.October 11,that year had a great surprise for him.It was his birthday and he had just returned home with his beautiful wife and twins after a visit to the famous Pittsburg temple. All his colleagues,including the head of NASA were standing in front of his house. He thought that they had just come to wish him but it turned out to be the day when Nobel Prize for Physics is announced every year. yes, he had won it that year. It seemed as though the whole universe was conspiring against him....................

It was a beautiful evening during the fall in the year 2015. A young energetic Indian graduate from Massachusetts Institute of Technology working for the NASA bumped upon some great idea during his evening stroll,which he did not realise then was goin to revolutionise the area of space travel.

Science had shrunken and now we live in the 'Femto world'.Nagarajan,popularly known as 'Mrinal' among his colleagues was working on 'picotechnology'. The word pico had replaced nano in all fields. Space travel was becoming more and more sophisticated but at the same time more and more complicated. It was at this time he was working with the fuel division in NASA. He struck upon the idea of picofuel cells matrixed in a layer of ceramic, which trapped 905 of solar enrgy and generated power for the shuttle. He presented his paper and got a great deal of appreciation. It as the days when space trave was limited to a particular distance due to fuel cost and expenditure. His idea passed all the prototypes and was asked to present the paper to the President of U.S.A. He approved it and funded 400 billion dollars for the project. he started working on the project and to everyone's surprise he and his team completed the project well ahead of time. The space shuttle with the new technology soared high into the sky during mid-October,2019.

Two years passed by and now he was heading the Far distance Space Exploration Division.October 11,that year had a great surprise for him.It was his birthday and he had just returned home with his beautiful wife and twins after a visit to the famous Pittsburg temple. All his colleagues,including the head of NASA were standing in front of his house. He thought that they had just come to wish him but it turned out to be the day when Nobel Prize for Physics is announced every year. yes, he had won it that year. It seemed as though the whole universe was conspiring against him....................

Friday, March 21, 2008

About My Self - S.SRIRAM

I am Sriram.S. Now I am working as a senior research consultant in IISc,Bangalore. I have 6 years experience in my field of research. I am a optimistic person with innovative thinking & ideas. My research mainly deals with implication of Nanotechnology in Astro physics. Being humourous, I am ready to face any stress situations with patience. If I imply my research works to your prestigious firm, it may be very useful to you. I have enough caliber to explore your company as a outstanding company. I wish to dedicate my research works to your firm.

Thursday, March 20, 2008

About myself-Deepika

I'm deepika,working as relations manager in Ford corp..I did my MBA in supply chain management.I have a previous experience of 5 years. I have worked on a project with a group of students from NUS,Singapore.The project mainly dealt with the development of tools and modules used for executing supply chain transactions,managing supplier relationships and controlling associated buisness processes. I have the stamina to work until the given task is accomplished and i wish to work in your company to make you a great competitor among various companies in global level.

Wednesday, March 19, 2008

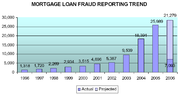

hi ppl.....dis article is abt d sub prime mortgage crisis in the US which is threatening to spiral into a global recession which is goig to affect each of us.....hope u find dis illuminating......

Number of U.S. Household Properties Subject to Foreclosure Actions During 2007, By Quarter

Number of U.S. Household Properties Subject to Foreclosure Actions During 2007, By Quarter  Existing Homes Sales, Inventory, and Months Supply, By Quarter

Existing Homes Sales, Inventory, and Months Supply, By Quarter

Borrowing Under a Securitization Structure

Borrowing Under a Securitization Structure

source:wiki...

The subprime mortgage crisis is an ongoing problem manifesting itself through liquidity issues in the banking system owing to foreclosures which accelerated in the United States in late 2006 and triggered a global financial crisis during 2007 and 2008. The crisis began with the bursting of the housing bubble in the US[2][3] and high default rates on "subprime" and other adjustable rate mortgages (ARM) made to higher-risk borrowers with lower income or lesser credit history than "prime" borrowers. Loan incentives and a long-term trend of rising housing prices encouraged borrowers to assume mortgages, believing they would be able to refinance at more favorable terms later. However, once housing prices started to drop moderately in 2006-2007 in many parts of the U.S., refinancing became more difficult. Defaults and foreclosure activity increased dramatically as ARM interest rates reset higher. During 2007, nearly 1.3 million U.S. housing properties were subject to foreclosure activity, up 79% versus 2006. [4] As of December 22, 2007, The Economist estimated subprime defaults would reach a level between U.S. $200-300 billion. [5]

The mortgage lenders that retained credit risk (the risk of payment default) were the first to be affected, as borrowers became unable or unwilling to make payments. Major banks and other financial institutions around the world have reported losses of approximately U.S. $170 billion as of February 2008, as cited below. Owing to a form of financial engineering called securitization, many mortgage lenders had passed the rights to the mortgage payments and related credit/default risk to third-party investors via mortgage-backed securities (MBS) and collateralized debt obligations (CDO). Corporate, individual and institutional investors holding MBS or CDO faced significant losses, as the value of the underlying mortgage assets declined. Stock markets in many countries declined significantly.

The widespread dispersion of credit risk and the unclear effect on financial institutions caused lenders to reduce lending activity or to make loans at higher interest rates. Similarly, the ability of corporations to obtain funds through the issuance of commercial paper was affected. This aspect of the crisis is consistent with a credit crunch. The liquidity concerns drove central banks around the world to take action to provide funds to member banks to encourage the lending of funds to worthy borrowers and to re-invigorate the commercial paper markets.

The subprime crisis also places downward pressure on economic growth, because fewer or more expensive loans decrease investment by businesses and consumer spending, which drive the economy. A separate but related dynamic is the downturn in the housing market, where a surplus inventory of homes has resulted in a significant decline in new home construction and housing prices in many areas. This also places downward pressure on growth. [6] With interest rates on a large number of subprime and other ARM due to adjust upward during the 2008 period, U.S. legislators and the U.S. Treasury Department are taking action. A systematic program to limit or defer interest rate adjustments was implemented to reduce the effect. In addition, lenders and borrowers facing defaults have been encouraged to cooperate to enable borrowers to stay in their homes. The risks to the broader economy created by the financial market crisis and housing market downturn were primary factors in the January 22, 2008 decision by the U.S. Federal reserve to cut interest rates and the economic stimulus package signed by President Bush on February 13, 2008. [7] [8] [9]Both actions are designed to stimulate economic growth and inspire confidence in the financial markets.

Contents[hide] |

[edit] Background information

Subprime lending is a general term that refers to the practice of making loans to borrowers who do not qualify for market interest rates because of problems with their credit history or the inability to prove that they have enough income to support the monthly payment on the loan for which they are applying. The word Subprime refers to the credit-worthiness of the borrower (being less than ideal) and does not refer to the interest rate of the loan. Subprime loans or mortgages are risky for both creditors and debtors because of the combination of high interest rates, bad credit history, and murky personal financial situations often associated with subprime applicants. A subprime loan is one that is offered at an interest rate higher than A-paper loans due to the increased risk. Subprime, therefore, is not the same as "Alt-A", because Alt-A loans qualify for the "A-rating" by Moody's or other rating firms, albeit for an "alternative" means.

The value of U.S. subprime mortgages was estimated at $1.3 trillion as of March 2007, [10] with over 7.5 million first-lien subprime mortgages outstanding. [11]Approximately 16% of subprime loans with adjustable rate mortgages (ARM) were 90-days delinquent or in foreclosure proceedings as of October 2007, roughly triple the rate of 2005. [12] By January of 2008, the delinquency rate had risen to 21%. [13]

Subprime ARMs only represent 6.8% of the loans outstanding in the US, yet they represent 43.0% of the foreclosures started during the third quarter of 2007. [14]A total of nearly 446,726 U.S. household properties were subject to some sort of foreclosure action from July to September 2007, including those with prime, alt-A and subprime loans. This is double the 223,000 properties in the year-ago period and 34% higher than the 333,627 in the prior quarter.[15] This increased to 527,740 during the fourth quarter of 2007, an 18% increase versus the prior quarter. For all of 2007, nearly 1.3 million properties were subject to 2.2 million foreclosure filings, up 79% and 75% respectively versus 2006. Foreclosure filings including default notices, auction sale notices and bank repossessions can include multiple notices on the same property.[16]

The estimated value of subprime adjustable-rate mortgages (ARM) resetting at higher interest rates is U.S. $400 billion for 2007 and $500 billion for 2008. Reset activity is expected to increase to a monthly peak in March 2008 of nearly $100 billion, before declining. [17] An average of 450,000 subprime ARM are scheduled to undergo their first rate increase each quarter in 2008. [18]

[edit] Understanding the causes and risks of the subprime crisis

The reasons for this crisis are varied and complex. [19] Understanding and managing the ripple effect through the world-wide economy poses a critical challenge for governments, businesses, and investors. Due to innovations in securitization, the risks related to the inability of homeowners to meet mortgage payments have been distributed broadly, with a series of consequential impacts. The crisis can be attributed to a number of factors, such as the inability of homeowners to make their mortgage payments; poor judgement by either the borrower or the lender; inappropriate mortgage incentives, and rising adjustable mortgage rates. Further, declining home prices have made re-financing more difficult. There are three primary categories of risk involved:

- Credit risk: Traditionally, the risk of default (called credit risk) would be assumed by the bank originating the loan. However, owing to innovations in securitization, credit risk is now shared more broadly with investors, because the rights to these mortgage payments have been repackaged into a variety of complex investment vehicles, generally categorized as mortgage-backed securities (MBS) or collateralized debt obligations (CDO). A CDO, essentially, is a repacking of existing debt, and in recent years MBS collateral has made up a large proportion of issuance. In exchange for purchasing the MBS, third-party investors receive a claim on the mortgage assets, which become collateral in the event of default. Further, the MBS investor has the right to cash flows related to the mortgage payments. To manage their risk, mortgage originators (e.g., banks or mortgage lenders) may also create separate legal entities, called special-purpose entities (SPE), to both assume the risk of default and issue the MBS. The banks effectively sell the mortgage assets (i.e., banking accounts receivable, which are the rights to receive the mortgage payments) to these SPE. In turn, the SPE then sells the MBS to the investors. The mortgage assets in the SPE become the collateral.

- Asset price risk: CDO valuation is complex and related "fair value" accounting for such "Level 3" assets is subject to wide interpretation. This valuation fundamentally derives from the collectibility of subprime mortgage payments, which is difficult to predict owing to lack of precedent and rising delinquency rates. Banks and institutional investors have recognized substantial losses as they revalue their CDO assets downward. Most CDOs require that a number of tests be satisfied on a periodic basis, such as tests of interest cash flows, collateral ratings, or market values. For deals with market value tests, if the valuation falls below certain levels, the CDO may be required by its terms to sell collateral in a short period of time, often at a steep loss, much like a stock brokerage account margin call. If the risk is not legally contained within an SPE or otherwise, the entity owning the mortgage collateral may be forced to sell other types of assets, as well, to satisfy the terms of the deal. In addition, credit rating agencies have downgraded over U.S. $50 billion in highly-rated CDO and more such downgrades are possible. Since certain types of institutional investors are allowed to only carry higher-quality (e.g., "AAA") assets, there is an increased risk of forced asset sales, which could cause further devaluation. [20]

- Liquidity risk: A related risk involves the commercial paper market, a key source of funds (i.e., liquidity) for many companies. Companies and SPE called structured investment vehicles (SIV) often obtain short-term loans by issuing commercial paper, pledging mortgage assets or CDO as collateral. Investors provide cash in exchange for the commercial paper, receiving money-market interest rates. However, because of concerns regarding the value of the mortgage asset collateral linked to subprime and Alt-A loans, the ability of many companies to issue such paper has been significantly affected. [21] The amount of commercial paper issued as of October 18, 2007 dropped by 25%, to $888 billion, from the August 8 level. In addition, the interest rate charged by investors to provide loans for commercial paper has increased substantially above historical levels. [22]

[edit] Understanding the effect on corporations and investors

Average investors and corporations face a variety of risks owing to the inability of mortgage holders to pay. These vary by legal entity. Some general exposures by entity type include:

- Bank corporations: The earnings reported by major banks are adversely affected by defaults on mortgages they issue and retain. Companies value their mortgage assets (receivables) based on estimates of collections from homeowners. Companies record expenses in the current period to adjust this valuation, increasing their bad debt reserves and reducing earnings. Rapid or unexpected changes in mortgage asset valuation can lead to volatility in earnings and stock prices. The ability of lenders to predict future collections is a complex task subject to a multitude of variables. [23]

- Mortgage lenders and Real Estate Investment Trusts: These entities face similar risks to banks. In addition, they have business models with significant reliance on the ability to regularly secure new financing through CDO or commercial paper issuance secured by mortgages. Investors have become reluctant to fund such investments and are demanding higher interest rates. Such lenders are at increased risk of significant reductions in book value owing to asset sales at unfavorable prices and several have filed bankruptcy. [24]

- Special purpose entities (SPE): Like corporations, SPE are required to revalue their mortgage assets based on estimates of collection of mortgage payments. If this valuation falls below a certain level, or if cash flow falls below contractual levels, investors may have immediate rights to the mortgage asset collateral. This can also cause the rapid sale of assets at unfavorable prices. Other SPE called structured investment vehicles (SIV) issue commercial paper and use the proceeds to purchase securitized assets such as CDO. These entities have been affected by mortgage asset devaluation. Several major SIV are associated with large banks. [25]

- Investors: Stocks or bonds of the entities above are affected by the lower earnings and uncertainty regarding the valuation of mortgage assets and related payment collection. Many investors and corporations purchased MBS or CDO as investments and incurred related losses.

[edit] Causes of the crisis

[edit] The housing downturn

- Further information: United States housing market correction

Subprime borrowing was a major contributor to an increase in home ownership rates and the demand for housing. The overall U.S. homeownership rate increased from 64 percent in 1994 (about where it was since 1980) to a peak in 2004 with an all time high of 69.2 percent.[26]

This demand helped fuel housing price increases and consumer spending. Between 1997 and 2006, American home prices increased by 124%. [27] Some homeowners used the increased property value experienced in the housing bubble to refinance their homes with lower interest rates and take out second mortgages against the added value to use the funds for consumer spending. U.S. household debt as a percentage of income rose to 130% during 2007, versus 100% earlier in the decade. [28] A culture of consumerism is a factor. In the early 2000s recession that began in early 2001 and which was exacerbated by the September 11, 2001 terrorist attacks, Americans were asked to spend their way out of economic decline with "consumerism... cast as the new patriotism". This call linking patriotism to shopping echoed the urging of former President Bill Clinton to "get out and shop" [29], and corporations like General Motors produced commercials with the same theme.

Overbuilding during the boom period, increasing foreclosure rates and unwillingness of many homeowners to sell their homes at reduced market prices have significantly increased the supply of housing inventory available. Sales volume (units) of new homes dropped by 26.4% in 2007 versus the prior year. By January 2008, the inventory of unsold new homes stood at 9.8 months based on December 2007 sales volume, the highest level since 1981. [30] Further, a record of nearly four million unsold existing homes were available. [31]

This excess supply of home inventory places significant downward pressure on prices. As prices decline, more homeowners are at risk of default and foreclosure. According to the S&P/Case-Shiller housing price index, by November 2007, average U.S. housing prices had fallen approximately 8% from their 2006 peak. [32]However, there was significant variation in price changes across U.S. markets, with many appreciating and others depreciating.[33] The price decline in December 2007 versus the year-ago period was 10.4%. As of February 2008, housing prices are expected to continue declining until this inventory of surplus homes (excess supply) is reduced to more typical levels.

[edit] Role of borrowers

A variety of factors have contributed to an increase in the payment delinquency rate for subprime ARM borrowers, which recently reached 21%, roughly four times its historical level. [34]

Easy credit, combined with the assumption that housing prices would continue to appreciate, also encouraged many subprime borrowers to obtain ARMs they could not afford after the initial incentive period. Once housing prices started depreciating moderately in many parts of the U.S. (see United States housing market correction and United States housing bubble), refinancing became more difficult. Some homeowners were unable to re-finance and began to default on loans as their loans reset to higher interest rates and payment amounts. Other homeowners, facing declines in home market value or with limited accumulated equity, are choosing to stop paying their mortgage. They are essentially "walking away" from the property and allowing foreclosure, despite the impact to their credit rating. [35]

Misrepresentation of loan application data is another contributing factor. In a January 13, 2008 column in the New York Times, George Mason University economics professor Tyler Cowen wrote, "There has been plenty of talk about 'predatory lending,' but 'predatory borrowing' may have been the bigger problem. As much as 70 percent of recent early payment defaults had fraudulent misrepresentations on their original loan applications, according to one recent study. The research was done by BasePoint Analytics, which helps banks and lenders identify fraudulent transactions; the study looked at more than three million loans from 1997 to 2006, with a majority from 2005 to 2006. Applications with misrepresentations were also five times as likely to go into default. Many of the frauds were simple rather than ingenious. In some cases, borrowers who were asked to state their incomes just lied, sometimes reporting five times actual income; other borrowers falsified income documents by using computers."[37]

US Department of the Treasury suspicious activity report of mortgage fraud increased by 1,411 percent between 1997 and 2005. [38]

[edit] Role of financial institutions

A variety of factors have caused lenders to offer an increasing array of higher-risk loans to higher-risk borrowers. The share of subprime mortgages to total originations was 5% ($35 billion) in 1994 [39] , 9% in 1996 [40], 13% ($160 billion) in 1999 [41] , and 20% ($600 billion) in 2006. [42][43] A study by the Federal Reserve indicated that the average difference in mortgage interest rates between subprime and prime mortgages (the "subprime markup" or "risk premium") declined from 2.8 percentage points (280 basis points) in 2001, to 1.3 percentage points in 2007. In other words, the risk premium required by lenders to offer a subprime loan declined. This occurred even though subprime borrower and loan characteristics declined overall during the 2001-2006 period, which should have had the opposite effect. The combination is common to classic boom and bust credit cycles. [44]

In addition to considering higher-risk borrowers, lenders have offered increasingly high-risk loan options and incentives. One example is the interest-only adjustable-rate mortgage (ARM), which allows the homeowner to pay just the interest (not principal) during an initial period. Another example is a "payment option" loan, in which the homeowner can pay a variable amount, but any interest not paid is added to the principal. Further, an estimated one-third of ARM originated between 2004-2006 had "teaser" rates below 4%, which then increased significantly after some initial period, as much as doubling the monthly payment. [45]

Some believe that mortgage standards became lax because of a moral hazard, where each link in the mortgage chain collected profits while believing it was passing on risk.[46]

[edit] Role of securitization

Securitization is a structured finance process in which assets, receivables or financial instruments are acquired, classified into pools, and offered as collateral for third-party investment.[47] There are many parties involved. Due to securitization, investor appetite for mortgage-backed securities (MBS), and the tendency of rating agencies to assign investment-grade ratings to MBS, loans with a high risk of default could be originated, packaged and the risk readily transferred to others. Asset securitization began with the structured financing of mortgage pools in the 1970s. [48] The securitized share of subprime mortgages (i.e., those passed to third-party investors) increased from 54% in 2001, to 75% in 2006. [49] Alan Greenspan stated that the securitization of home loans for people with poor credit — not the loans themselves — were to blame for the current global credit crisis. [50]

[edit] Role of mortgage brokers

Mortgage brokers don't lend their own money. There is not a direct correlation between loan performance and compensation. They have big financial incentives for selling complex, adjustable rate mortgages (ARM's), since they earn higher commissions. [51]

According to a study by Wholesale Access Mortgage Research & Consulting Inc., in 2004 Mortgage brokers originated 68% of all residential loans in the U.S., with subprime and Alt-A loans accounting for 42.7% of brokerages' total production volume. [52]

The chairman of the Mortgage Bankers Association claimed brokers profited from a home loan boom but didn't do enough to examine whether borrowers could repay. [53]

[edit] Role of mortgage underwriters

Underwriters determine if the risk of lending to a particular borrower under certain parameters is acceptable. Most of the risks and terms that underwriters consider fall under the three C’s of underwriting: credit, capacity and collateral. See mortgage underwriting.

In 2007, 40 percent of all subprime loans were generated by automated underwriting. [54] An Executive vice president of Countrywide Home Loans Inc. stated in 2004 "Prior to automating the process, getting an answer from an underwriter took up to a week. "We are able to produce a decision inside of 30 seconds today. ... And previously, every mortgage required a standard set of full documentation."[55] Some think that users whose lax controls and willingness to rely on shortcuts led them to approve borrowers that under a less-automated system would never have made the cut are at fault for the subprime meltdown. [56]

[edit] Role of government and regulators

Some economists claim that government policy actually encouraged the development of the subprime debacle through legislation like the Community Reinvestment Act, which they say forces banks to lend to otherwise uncreditworthy consumers.[57] [58] Economist Robert Kuttner has criticized the repeal of the Glass-Steagall Act as contributing to the subprime meltdown. [59] A taxpayer-funded government bailout related to mortgages during the Savings and Loan crisis may have created a moral hazard and acted as encouragement to lenders to make similar higher risk loans. [60]

Some have argued that, despite attempts by various U.S. states to prevent the growth of a secondary market in repackaged predatory loans, the Treasury Department's Office of the Comptroller of the Currency, at the insistence of national banks, struck down such attempts as violations of Federal banking laws.[61]

In response to a concern that lending was not properly regulated, the House and Senate are both considering bills to regulate lending practices. [62]

[edit] Role of credit rating agencies

Credit rating agencies are now under scrutiny for giving investment-grade ratings to securitization transactions holding subprime mortgages. Higher ratings are theoretically due to the multiple, independent mortgages held in the MBS per the agencies, but critics claim that conflicts of interest were in play.

[edit] Role of central banks

Central banks are primarily concerned with managing the rate of inflation and avoiding recessions. They are also the “lenders of last resort” to ensure liquidity. They are less concerned with avoiding asset bubbles, such as the housing bubble and dotcom bubble. Central banks have generally chosen to react after such bubbles burst to minimize collateral impact on the economy, rather than trying to avoid the bubble itself. This is because identifying an asset bubble and determining the proper monetary policy to properly deflate it are not proven concepts. [63] There is significant debate among economists regarding whether this is the optimal strategy. [64]

Federal Reserve actions raised concerns among some market observers that it could create a moral hazard. Some industry officials said that Federal Reserve Bank of New York involvement in the rescue of Long-Term Capital Management in 1998 would encourage large financial institutions to assume more risk, in the belief that the Federal Reserve would intervene on their behalf. [65]

A potential contributing factor to the rise in home prices was the lowering of interest rates earlier in the decade by the Federal Reserve, to diminish the blow of the collapse of the dot-com bubble and combat the risk of deflation. [66]

[edit] Effects

Company  | Business Type | Loss (Billion $) |

|---|---|---|

| investment bank | $24.1 bln [67] [68] [69] | |

| investment bank | $22.5 bln [70] [71] | |

| investment bank | $18.7 bln [72] [73] | |

| investment bank | $10.3 bln [74] [75] | |

| bank | $4.8 bln [76] | |

| bank | $17.2 bln [77][78] | |

| bank | $9.4 bln [79] | |

| bank | $3.2 bln [80] | |

| investment bank | $3.1 bln [81] [82] | |

| investment bank | $3.1 bln [83] | |

| investment bank | $2.6 bln [84] [85] | |

| bank | $3.5 bln [86][87][88] | |

| savings and loan | $2.4 bln [89] [90] | |

| re-insurance | $1.07 bln [91] | |

| investment bank | $2.1 bln [92] [93] | |

| bank | $1.1 bln [94] | |

| investment bank | $2.9 bln [95] [96] | |

| investment bank | $1.5 bln [97] [98] | |

| mortgage GSE | $3.6 bln [99] [100] | |

| bank | $3.7 bln [101] | |

| bank | $1.4 bln [102] | |

| bank | $3.0 bln [103] [104] | |

| bank | $0.360 bln [105] [106] | |

| mortgage GSE | $0.896 bln [107] | |

| bond insurance | $3.3 bln [108] | |

| bank | $0.580 bln [109] | |

| bond insurance | $3.5 bln [110] [111] [112] | |

| bank | $1.1 bln [113] | |

| investment bank | $3.0 bln [114] [115] | |

| bank | $0.870 bln [116] [117] | |

| bank | $1.37 bln [118] [119] | |

| insurance | $11.1 bln [120][121] | |

| bank | $2.8 bln [122] | |

| bank | $1.75 bln [123] | |

| mortgage bank | $1.0 bln [124] | |

| bank | $2.1 bln [125] | |

| bank | $2.3 bln [126] | |

| bank | $0.264 bln [127] |

| Business | Type | Date |

|---|---|---|

| subprime lender | April 2, 2007 | |

| mortgage lender | August 6, 2007 | |

| investment fund | August 17, 2007 [128] | |

| subprime lender | August 31, 2007 | |

| on-line bank | September 30, 2007[129] | |

| securities | November 28, 2007 [130] | |

| subprime lender | January 30, 2007 [131] |

In addition, Northern Rock and Bear Stearns[132] have required emergency government bailouts.

[edit] Effect on stock markets

On July 19, 2007, the Dow Jones Industrial Average hit a record high, closing above 14,000 for the first time. [133] By August 15, the Dow had dropped below 13,000 and the S&P 500 had crossed into negative territory year-to-date. Similar drops occurred in virtually every market in the world, with Brazil and Korea being hard-hit. Large daily drops became common, with, for example, the KOSPI dropping about 7% in one day, [134] although 2007's largest daily drop by the S&P 500 in the U.S. was in February, a result of the subprime crisis.

Mortgage lenders [135] [136] and home builders [137] [138] fared terribly, but losses cut across sectors, with some of the worst-hit industries, such as metals & mining companies, having only the vaguest connection with lending or mortgages. [139]

[edit] Effect on financial institutions

- See also: Subprime crisis impact timeline

Many banks, mortgage lenders, real estate investment trusts (REIT), and hedge funds suffered significant losses as a result of mortgage payment defaults or mortgage asset devaluation. As of March 16, 2008 financial institutions had recognized subprime-related losses or write-downs exceeding U.S. $175 billion.

Profits at the 8,533 U.S. banks insured by the FDIC declined from $35.2 billion to $5.8 billion (83.5 percent) during the fourth quarter of 2007 versus the prior year, due to soaring loan defaults and provisions for loan losses. It was the worst bank and thrift performance since the fourth quarter of 1991. For all of 2007, these banks earned $105.5 billion, down 27.4 percent from a record profit of $145.2 billion in 2006.[140]

Other companies from around the world, such as IKB Deutsche Industriebank [141], have also suffered significant losses [142] and scores of mortgage lenders have filed for bankruptcy. [143] Top management has not escaped unscathed, as the CEOs of Merrill Lynch and Citigroup were forced to resign within a week of each other. [144] Various institutions follow-up with merger deals.[145]

The crisis also affected Indian banks which have ventured into USA. ICICI, India's second largest bank, has reported mark-to-market loss of $263 million in its loans and investment exposures. Other state owned banks such as State Bank of India, Bank of India and Bank of Baroda have refused to release their figures. [146]

[edit] Effect on insurance companies

There is concern that some homeowners are turning to arson as a way to escape from mortgages they can't or refuse to pay. The FBI reports that arson grew 4% in suburbs and 2.2% in cities from 2005 to 2006. As of Jan 2008, the 2007 numbers were not yet available. [147] [148]

[edit] Effect on municipal bond "monoline" insurers

A secondary cause and effect of the crisis relates to the role of municipal bond "monoline" insurance corporations. By insuring municipal bond issues, those bonds achieve higher debt ratings. However, these insurers used premiums to purchase CDO investments and have suffered significant losses, which brings their ability to insure bonds into question. Unless these insurers obtain additional capital, rating agencies may downgrade the bonds they insured or guaranteed. In turn, this may require financial institutions holding the bonds to lower their valuation or to sell them, as some entities (such as pension funds) are only allowed to hold the highest-grade bonds. The effect of such a devaluation on institutional investors and corporations holding the bonds (including major banks) has been estimated as high as $200 billion. Regulators are taking action to encourage banks to lend the required capital to certain monoline insurers, to avoid such an impact. [149]

[edit] Effect on home owners

- Further information: United States housing market correction

According to the S&P/Case-Shiller housing price index, by November 2007, average U.S. housing prices had fallen approximately 8% from their 2006 peak. [150]However, there was significant variation in price changes across U.S. markets, with many appreciating and others depreciating.[151] The price decline in December 2007 versus the year-ago period was 10.4%. Sales volume (units) of new homes dropped by 26.4% in 2007 versus the prior year. By January 2008, the inventory of unsold new homes stood at 9.8 months based on December 2007 sales volume, the highest level since 1981. [152]

Housing prices are expected to continue declining until this inventory of surplus homes (excess supply) is reduced to more typical levels. As MBS and CDO valuation is related to the value of the underlying housing collateral, MBS and CDO losses will continue until housing prices stabilize. [153]

As home prices have declined following the rise of home prices caused by speculation and as re-financing standards have tightened, a number of homes have been foreclosed and sit vacant. These vacant homes are often poorly-maintained and sometimes attract squatters and/or criminal activity with the result that increasing foreclosures in a neighborhood often serve to further accelerate home price declines in the area. Rents have not fallen as much as home prices with the result that in some affluent neighborhoods homes that were formerly owner occupied are now occupied by renters. In select areas falling home prices along with a decline in the U.S. dollar have encouraged foreigners to buy homes for either occasional use and/or long term investments. Additional problems are anticipated in the future from the impending retirement of the baby boomer generation. It is believed that a significant proportion of baby boomers are not saving adequately for retirement and were planning on using their increased property value as a "piggy bank" or replacement for a retirement-savings account. This is a departure from the traditional American approach to homes where "people worked toward paying off the family house so they could hand it down to their children" [154].

[edit] Effect on minorities

There is a disproportionate level of foreclosures in some minority neighborhoods. [155] [156]

About 46% of Hispanics and 55% of blacks who obtained mortgages in 2005 got higher-cost loans compared with about 17% of whites and Asians, according to Federal Reserve data. Other studies indicate they would have qualified for lower-rate loans. [157]

[edit] Actions to manage the crisis

- Lenders and homeowners both may benefit from avoiding foreclosure, which is a costly and lengthy process. Some lenders have taken action to reach out to homeowners to provide more favorable mortgage terms (i.e., loan modification or refinancing). Homeowners have also been encouraged to contact their lenders to discuss alternatives. [158] Corporations, trade groups, and consumer advocates have begun to cite statistics on the numbers and types of homeowners assisted by loan modification programs. There is some dispute regarding the appropriate measures, sources of data, and adequacy of progress. A report issued in January 2008 showed that mortgage lenders modified 54,000 loans and established 183,000 repayment plans in the third quarter of 2007, a period in which there were 384,000 new foreclosures. Consumer groups claimed the modifications affected less than 1 percent of the 3 million subprime loans with adjustable rates that were outstanding in the third quarter. [159]

- Credit rating agencies help evaluate and report on the risk involved with various investment alternatives. The rating processes can be re-examined and improved to encourage greater transparency to the risks involved with complex mortgage-backed securities and the entities that provide them. Rating agencies have recently begun to aggressively downgrade large amounts of mortgage-backed debt. [160]

- Regulators and legislators can take action regarding lending practices, bankruptcy protection, tax policies, affordable housing, credit counseling, education, and the licensing and qualifications of lenders. [161] Regulations or guidelines can also influence the nature, transparency and regulatory reporting required for the complex legal entities and securities involved in these transactions. Congress also is conducting hearings help identify solutions and apply pressure to the various parties involved. [162]

- The media can help educate the public and parties involved. [163] It can also ensure the top subject material experts are engaged and have a voice to ensure a reasoned debate about the pros and cons of various solutions. [164]

- Banks have sought and received additional capital (i.e., cash investments) from sovereign wealth funds, which are entities that control the surplus savings of developing countries. An estimated U.S. $69 billion has been invested by these entities in large financial institutions over the past year. On January 15, 2008, sovereign wealth funds provided a total of $21 billion to two major U.S. financial institutions. Such capital is used to help banks maintain required capital ratios (an important measure of financial health), which have declined significantly due to subprime loan or CDO losses. Sovereign wealth funds are estimated to control nearly $2.9 trillion. Much of this wealth is oil and gas related. As they represent the surplus funds of governments, these entities carry at least the perception that their investments have underlying political motives. [165]

- Litigation related to the subprime crisis is underway. A study released in February 2008 indicated that 278 civil lawsuits were filed in federal courts during 2007 related to the subprime crisis. The number of filings in state courts were not quantified but are also believed to be significant. The study found that 43 percent of the cases were class actions brought by borrowers, such as those that contended they were victims of discriminatory lending practices. Other cases include securities lawsuits filed by investors, commercial contract disputes, employment class actions, and bankruptcy-related cases. Defendants included mortgage bankers, brokers, lenders, appraisers, title companies, home builders, servicers, issuers, underwriters, bond insurers, money managers, public accounting firms, and company boards and officers. [166]

[edit] Bush Administration plan

President George W. Bush announced a plan voluntarily and temporarily to freeze the mortgages of a limited number of mortgage debtors holding ARMs, declaring "I have a message for every homeowner worried about rising mortgage payments: The best you can do for your family is to call 1-800-995-HOPE (sic)" [167]. The correct number is 1-888-995-HOPE.[168]. A refinancing facility called FHA-Secure was also created. [169] This is part of an ongoing collaborative effort between the US Government and private industry to help some sub-prime borrowers called the Hope Now Alliance.[170]

The Hope Now Alliance released a report in February, 2008 indicating it helped 545,000 subprime borrowers with shaky credit in the second half of 2007, or 7.7 percent of 7.1 million subprime loans outstanding in September 2007. A spokesperson acknowledged that much more must be done. [171]

During February 2008, a program called "Project Lifeline" was announced. Six of the largest U.S. lenders, in partnership with the Hope Now Alliance, agreed to defer foreclosure actions for 30 days for homeowners 90 or more days delinquent on payments. The intent of the program was to encourage more loan adjustments, to avoid foreclosures. [172]

The U.S. Treasury Department is working directly with major banks to develop a systematic means of modifying loans for a significant portion of borrowers facing ARM increases, rather than working through loans on a case-by-case basis. [173]

President Bush also signed into law on February 13, 2008 an economic stimulus package of $168 billion, mainly in the form of income tax rebates, to help stimulate economic growth. [174]

[edit] The Federal Reserve

Federal Reserve Chairman Ben Bernanke signaled towards making interest rate cuts. In early 2008, Ben Bernanke said: "Broadly, the Federal Reserve’s response has followed two tracks: efforts to support market liquidity and functioning and the pursuit of our macroeconomic objectives through monetary policy." [175] Tougher regulatory standards are proposed. Additionally, a freeze of interest payments on certain sub-prime loans is announced.[176] On January 22, 2008, the Fed also slashed a key interest rate (the federal funds rate) by 75 basis points to 3.5%, the biggest cut since 1984, followed by another cut of 50 basis points on January 30th.[177]

The Fed and other central banks have conducted open market operations to ensure member banks have access to funds (i.e., liquidity). These are effectively short-term loans to member banks collateralized by government securities. Central banks have also lowered the interest rates charged to member banks (called the discount rate in the U.S.) for short-term loans. [178] Both measures effectively lubricate the financial system, in two key ways. First, they help provide access to funds for those entities with illiquid mortgage-backed assets. This helps lenders, SPE, and SIV avoid selling mortgage-backed assets at a steep loss. Second, the available funds stimulate the commercial paper market and general economic activity. Specific responses by central banks are included in the subprime crisis effect timeline.

The Fed is utilizing the Term auction facility (TAF) to provide short-term loans (liquidity) to banks. The Fed increased the monthly amount of these auctions to $100 billion during March 2008, up from $60 billion in prior months. In addition, term repurchase agreements expected to cumulate to $100 billion were announced, which enhance the ability of financial institutions to sell mortgage-backed and other debt. The Fed indicated that both the TAF and repurchase agreement amounts will continue and be increased as necessary.[179]

Fed Chairman Bernanke also delivered a speech March 4, 2008 titled "Reducing Preventable Mortgage Foreclosures." He advocated several solutions, including the reduction of loan principal amounts.[180] This solution was highlighted to address a growing concern that an estimated 8.8 million U.S. homeowners (10%) with negative equity (homes worth less than the mortgage principal) will have a financial incentive to "walk away" from the property, further exacerbating the crisis.[181]

In March 2008, the Fed also provided funds and guarantees to enable bank J.P. Morgan Chase to purchase Bear Stearns, a large financial institution with substantial mortgage-backed securities (MBS) investments that had recently plunged in value. This action was taken in part to avoid a potential fire sale of nearly U.S. $210 billion of Bear Stearns' MBS and other assets, which could have caused further devaluation in similar securities across the banking system, potentially destabilizing other major financial institutions.[182][183]

[edit] Expectations and forecasts

As early as the 2003 Annual Report issued by Fairfax Financial Holdings Limited, Prem Watsa was raising concerns about securitized products:

| “ | We have been concerned for some time about the risks in asset-backed bonds, particularly bonds that are backed by home equity loans, automobile loans or credit card debt (we own no asset-backed bonds). It seems to us that securitization (or the creation of these asset-backed bonds) eliminates the incentive for the originator of the loan to be credit sensitive. Take the case of an automobile dealer. Prior to securitization, the dealer would be very concerned about who was given credit to buy an automobile. With securitization, the dealer (almost) does not care as these loans can be laid off through securitization. Thus, the loss experienced on these loans after securitization will no longer be comparable to that experienced prior to securitization (called a ‘‘moral’’ hazard)... This is not a small problem. There is $1.0 trillion in asset-backed bonds outstanding as of December 31, 2003 in the U.S. … Who is buying these bonds? Insurance companies, money managers and banks – in the main – all reaching for yield given the excellent ratings for these bonds. What happens if we hit an air pocket? Unlike…[184] | ” |

The legacy of Alan Greenspan has been cast into doubt with Senator Chris Dodd claiming he created the "perfect storm" [185]. Alan Greenspan has remarked that there is a one-in-three chance of recession from the fallout. Nouriel Roubini, a professor at New York University and head of Roubini Global Economics, has said that if the economy slips into recession "then you have a systemic banking crisis like we haven't had since the 1930s" [186].

On September 7, 2007, the Wall Street Journal reported that Alan Greenspan has said that the current turmoil in the financial markets is in many ways "identical" to the problems in 1987 and 1998.[187]

The Associated Press described the current climate of the market on August 13, 2007, as one where investors were waiting for "the next shoe to drop" as problems from "an overheated housing market and an overextended consumer" are "just beginning to emerge."[not in citation given] MarketWatch has cited several economic analysts with Stifel Nicolaus claiming that the problem mortgages are not limited to the subprime niche saying "the rapidly increasing scope and depth of the problems in the mortgage market suggest that the entire sector has plunged into a downward spiral similar to the subprime woes whereby each negative development feeds further deterioration", calling it a "vicious cycle" and adding that they "continue to believe conditions will get worse" [188].

Citigroup economists stated in mid-March 2008 regarding the likelihood of a recession that “The self-feeding downturn now in place shows signs of becoming deeply entrenched.”[189]

As of November 22, 2007, analysts at a leading investment bank estimated losses on subprime CDO would be approximately U.S. $148 billion. [190] As of December 22, 2007, a leading business periodical estimated subprime defaults between U.S. $200-300 billion. [191] As of March 1, 2008 analysts from three large financial institutions estimated the impact would be between U.S. $350-600 billion.[192]

Alan Greenspan, the former Chairman of the Federal Reserve, stated: "The current credit crisis will come to an end when the overhang of inventories of newly built homes is largely liquidated, and home price deflation comes to an end. That will stabilize the now-uncertain value of the home equity that acts as a buffer for all home mortgages, but most importantly for those held as collateral for residential mortgage-backed securities. Very large losses will, no doubt, be taken as a consequence of the crisis. But after a period of protracted adjustment, the U.S. economy, and the world economy more generally, will be able to get back to business.source:wiki...

Subscribe to:

Posts (Atom)